?What are balanced scorecards

*Written by: Zaher Basheer Al Abdo

Strategic management thinker, writer, and researcher in institutional development.

What are balanced scorecards?

#Kaplan and #Norton‘s 1992 article in the #Harvard Business Review titled “The #Balanced_Scorecard for Measuring Performance Motivation” was an important reason for the journal’s increase in sales, and subsequently, “The Balanced Scorecard: Translating Strategy into Action” published in 1996

The results of #financial performance are a reflection of the mechanisms and method of dealing with funds within #organizations, which are important even in non-profit organizations. However, evaluating the results of organizations’ work according to financial indicators only suffers from shortcomings on the one hand:

1. Historical approach: It analyses the results of what has been done and ended and does not consider what is happening now or in the future.

2. Insufficient approach: because it does not measure the value of intangible assets.

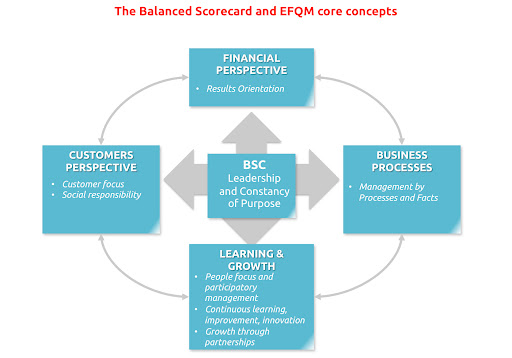

That is why the balanced scorecards perspectives presented by Kaplan and Norton came as a strategic approach and a standard for management performance capable of translating the organization’s vision and strategy into an application based on four perspectives: “financial – customer – learning and growth – business processes” so that these perspectives allow in monitoring and measuring current performance to control achievement in the future.

In other words, the balanced scorecard provides the organization with tools for evaluating performance from various aspects of its activity and business results, as it adjusts the components of the goals groups that the organization seeks to achieve, and therefore the cards are a translation of the organization’s vision, mission, strategy, and strategic direction, as they produce exact goals with standards and indicators according to the four dimensions of each of them. According to a different perspective, i.e., multi-objective monitoring in planning, implementation, and development according to the PDD institutional excellence approach to measure overall performance from those four perspectives, as follows:

- First: the financial perspective: The BSC approach has not overlooked the importance of the traditional need to monitor business results for accurate financial data. This perspective includes financial objectives such as: profitability, return on investment, product cost, cash flow, and is used to measure this financial ratios and various financial figures, and may Some see that these indicators are not important for organizations and institutions that do not aim for profit, such as charities and humanitarian organizations, but the reality is otherwise, even if it is not for profit, it must take into account the financial indicators and ways to control them in order to maintain the continuity of their activities and their distribution in order to achieve the best return according to its objectives.

- Second: The customer’s perspective: The reality of the buyers’ market as a concept that drives the philosophy of modern management, on the one hand, that the customer will look for another supplier in the event that the company does not succeed in gaining his satisfaction and loyalty, and therefore the low performance of customer satisfaction is a regressive indicator despite the lack of a financial picture that may seem good In the short term, therefore, the analysis of reports on the types of customers and their level of satisfaction, trends and desires is crucial to the success of the organization, and for this the organization should direct its attention to studying the orientation of its customers and meet their needs and desires because they are the main source of income for the organization to cover the costs of providing its products / services in the first place and achieve Profits are in the second place, and therefore, according to this perspective, goals and indicators must be set that reflect the position of customers in relation to the organization, such as: the degree of loyalty, customer satisfaction, market share, the ability to attract the customer, customer profitability, and the ability to retain customers.

- Third: The Learning and Growth Perspective: The components of the objectives and criteria for measuring this perspective are related to the capabilities that the organization must achieve in terms of individual competencies and core competencies in order to ensure work according to activities and operational plans capable of creating value and benefits for PRH owners, by focusing on the following three basic aspects:

- Creating the capabilities of the workers and controlling their direction to ensure the provision of useful and renewable knowledge and the provision of ways and tools for its investment that generates useful experiences that create an environment of creativity, improvement and continuous development, and this is done through education and development of workers within a well-studied interactive learning plan on the one hand, and measuring the level of employee satisfaction on the one hand, loyalty on the second hand, and their productivity on the third.

- Follow up, measure, and develop the efficiency and effectiveness of information systems, in order to ensure the provision of correct and accurate scheduling, classification and sorting of data and then analyzing them in order to reach information capable of drawing trends that support decision makers and decision takers in developing the results of the organization’s work on the one hand, and overcoming the problems that stand in the way of its work on the other hand.

- Ensuring the creation of incentive and delegation programs and the accountability of employees. This approach ensures greater effectiveness of business results, as it constitutes one of the three pillars of successful leadership, especially after setting goals at all levels and providing tools and requirements to achieve them and ensuring the understanding of implementation mechanisms for those concerned with them.

- Fourth: The perspective of the business process and internal systems: This perspective is integrated with the contents of the previous two perspectives in terms of qualifying and training workers and directing the organization’s behaviour and its organizational and administrative culture.

It is important to follow up on measuring the organization’s internal systems to ensure the provision of a competitive environment among them, the most important of which are:

- Renewal system: especially with regard to research and development, the number of patents, and the number of new products.

- Production system: especially with regard to the quality of products, and production deadlines.

- After-sales service system: especially customer reception skills, and problem-solving controls.

In this context, it is necessary to emphasize the importance of integrating initiatives, activities, programmes, projects, and plans, when possible, in a way that ensures saving time and expenditures without affecting the quality of the outputs, bearing in mind that success in creating integration between the outputs of the four perspectives is extremely important in strengthening the situation Competitiveness and achieving and maintaining competitive advantage.

What are the shortcomings that need to be addressed?

We can see the shortcomings of BSC Balanced Scorecards from two main aspects:

The origin of its concept is based on the components of Hoshin Kanri based on the concept of industrial quality in the first place, without expanding to suit administrative processes in a way that enhances its importance and diversity, and its inclusion in the rest of the controls of the needs of the positive role holders PRH.

Not taking them into account structurally, in what is appropriate for government service organizations in general, especially those associations and non-profit organizations, where the financial perspective becomes much less important than it is in profit organizations in general and business organizations in particular.

***

The original article is from the author’s website at the following link

https://lnkd.in/diwPq3xa

***

#management#motivation#hr

https://lnkd.in/g_KxYhNk

#HigherInstituteOfScienceAndTechnologyResearch

#dailymotivation#onlinetraining

#corporatetraininginstitute#dubai