Zaher Bashir Al Abdo Strategic Management Thinker Award in Applied Management

للمزيد عن هذه الجائزة فضلاً راجع التفاصيل ف الرابط أدناه من موقع منظمة الإدارة العربية

https://amo1.org/zaher-basheer-al-abdo-award-for-strategic-management/

The Honor Chief of the Arab Management Org. | The Inventor ”MBI” Theory, the ”Leadership_21” Approach and ISS strategy.

Zaher Bashir Al Abdo Strategic Management Thinker Award in Applied Management

للمزيد عن هذه الجائزة فضلاً راجع التفاصيل ف الرابط أدناه من موقع منظمة الإدارة العربية

https://amo1.org/zaher-basheer-al-abdo-award-for-strategic-management/

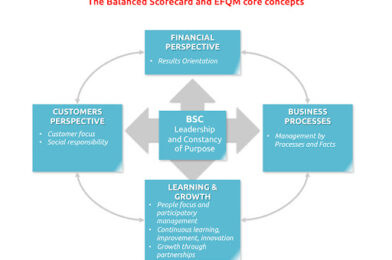

ما هي بطاقات الأداء المتوازن؟

كانت مقالة كابلن ونورتن المنشورة عام 1992 في دورية “هارفارد للأعمال” بعنوان “بطاقة الإداء المتوازن لقياس دوافع الأداء” سبباً مهماً في زيادة مبيعات الدورية، ومن ثم “بطاقة قياس الأداء المتوازنة: ترجمة الاستراتيجية لفعل” التي نشرت عام 1996

تعتبر نتائج الأداء المالي انعكاس لآليات وأسلوب التعامل مع الأموال داخل المنظمات، وهي ذات أهمية حتى في المنظمات غير الربحية، إلا أن تقييم نتائج أعمال المنظمات وفق المؤشرات المالية فقط يعاني من قصور من جهة:

ولهذا جاءت مناظير بطاقات الأداء المتوازن التي قدمها كابلن ونورتن كمنهج استراتيجي ومعيار لأداء الإدارة قادر على ترجمة رؤية المنظمة واستراتيجيتها الى تطبيق يقوم على أربعة مناظير هي ” المالي – العميل – التعلم والنمو – عميات الاعمال” بحيث تسمح هذه المناظير في رصد وقياس الأداء الحالي لضبط الإنجاز بالمستقبل.

بمعنى آخر فإن بطاقة الأداء المتوازن توفر للمنظمة أدوات تقييم الأداء من مختلف جوانب نشاطها ونتائج أعمالها، حيث تقوم بضبط مكونات مجموعات الأهداف التي تسعى المنظمة لتحقيقها، وبالتالي فالبطاقات هي ترجمة لرؤية المنظمة ورسالتها واستراتيجيتها وتوجهها الاستراتيجي تنتج نها أهداف مضبوطة بمقاييس ومؤشرات وفق الأبعاد الأربعة كل منها وفق منظور مختلف، أي رصد متعدد الأهداف في التخطيط والتنفيذ والتطوير وفق منهج التميز المؤسسي PDD لقياس الأداء الكلي من تلك المناظير الأربعة، وفق ما يلي:

ولابد في هذا السياق من التأكيد على أهمية دمج المبادرات والأنشطة والبرامج والمشاريع والخطط عندما يمكن ذلك بما يضمن تحقيق وفر بالوقت والنفقات دون التأثير على جودة المخرجات، مع الأخذ بعين الاعتبار أن النجاح في خلق التكامل بين مخرجات المناظير الأربعة هو أمر في غاية الأهمية في تعزيز الموقف التنافسي وتحقيق الميزة التنافسية والمحافظة عليها.

ثالثاً: ما هو القصور الواجب معالجته؟

يمكننا تلمس قصور بطاقات الأداء المتوازن BSC من جهتين أساسيتين هما:

What is Hoshin_Kanri?

Written by: Zaher Basheer Al Abdo*

*Strategic management thinker, writer, and researcher in institutional development.

This proposition comes as a continuation of what I discussed in this regard in my book “Integration or Death.. Strategic Management by Integration #MBI, 2018”, where I discussed in the first topic of Chapter Eight under the title “What are the deficiencies of KPI’s performance indicators” by Parmenter after we found that the foundations of scorecards Balanced #BSC introduced by #Kaplan and #Norton drew its roots from the Japanese concept of #Hoshin_Kanri.

In fact, what made me go back to talking about this subject before the publication of my book ” #Indicators of #Institutional #Excellence and #Strategic #Development” were two things that made me discuss this content with experienced and specialized people in order to take into account the results of that in my next book.

Since this topic is based on important basic concepts, I found that I reformulated those concepts in useful and brief terms to benefit from them in building what I would like to present from an applied intellectual development in this context.

First: What is Hoshin Kanri?

Hoshin’s philosophy was first introduced in the sixties of the last century within the #management practices of #Toyota, #Bridgestone, #Nabibone, and others as a result of working according to the content of the #PDCA #Deming_circle on the one hand, and the content of management with the goals presented by #Peter_Drucker, and the propositions of #Juran, after that the applied concept of Hoshin developed during the seventies Up to what was published by the #Japan_Standards_Association for a series of works based on Hoshin practices in 1988, and the Hoshin application moved to America in the eighties and was applied with special models from Hoshin Kanri in each of #Xerox, #Procter & Campbell, and #Hewlett Packard…

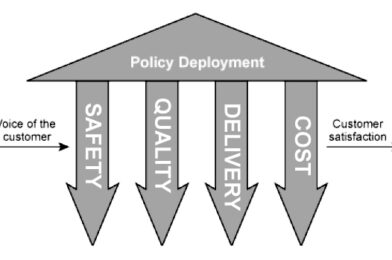

The basis of the Hoshin plan is based on reviewing the results of the previous year to build the new plan, provided that it includes a series of activities of the organization within periodic planning tables, where the results of implementation are reviewed in comparison with what is planned to make the appropriate correction or improvement, and Hoshin planning can be expressed as employing the #quality policy in the #organization.

The difficulty of applying Hoshin in some organizations is due to the necessity of strict application, long-term commitment and continuous support from senior management, because the goals of penetration must be stable for five years. Using measurement standards that monitor implementation to ensure continuity of continuous improvement of the organization’s core operations.

Note that the Japanese concept of Kanri is a management concept that expresses periodic planning and is applied at two levels:

ما هي هوشين كانري[1]

بقلم: زاهر بشير العبدو*

*مفكر إدارة استراتيجي، كاتب، باحث في التطوير المؤسسي.

يأتي هذا الطرح استكمالاً لما ناقشته بهذا الخصوص في كتابي “التكامل أو الفناء.. الإدارة الاستراتيجية بالتكامل، 2018” حيث ناقشت فيه بالمبحث الأول من الفصل الثامن تحت عنوان “ما أوجه قصور مؤشرات الأداء KPI’s” عند بارمنتر Parmenter بعد ان وجدنا أن مرتكزات بطاقات الأداء المتوازن BSC التي قدمها كابلان ونورتن استمدت جذورها من مفهوم هوشين كانري الياباني.

في الحقيقة ما جعلني أعود للحديث عن هذا الموضوع قبل صدور كتابي “مؤشرات التميز المؤسسي والتطوير الاستراتيجي” هو أمرين جعلاني اناقش هذا المضمون مع أهل التجربة والاختصاص كي آخذ بعين الاعتبار نتائج ذلك في كتابي القادم.

وحيث أن هذا الموضوع يستند على مفاهيم أساسية مهمة، فقد وجدت أن أعيد صياغة تلك المفاهيم في عبارات مفيدة ومختصرة لأستفيد منها في بناء ما أود تقديمه من تطوير فكري تطبيقي في هذا السياق.

ما هي هوشين كانري؟[2]

كان أول طرح لفلسفة هوشين في ستينيات القرن الماضي ضمن ممارسات الإدارة في شركة تويوتا، بريدجستون، نبيبون.. وغيرها كنتيجة للعمل وفق مضمون دائرة ديمنغ PDCA من جهة ومضمون الإدارة بالأهداف التي قدمها بيتر دراكر، وطروحات جوران، بعد ذلك تطور المفهوم التطبيقي لهوشين خلال السبعينيات وصولاً لما نشرته الجمعية اليابانية للمعايير لسلسلة الأعمال التي ترتكز على ممارسات هوشين عام 1988، وانتقل تطبيق هوشين الى أمريكا في الثمانينات وطبق بنماذج خاصة من هوشين كانري في كل من زيروكس وبروكتر اند كامبل وهيولت باكارد …

يرتكز أساس خطة هوشين على مراجعة نتائج السنة السابقة لبناء الخطة الجديدة على أن تتضمن سلسلة من أنشطة المنظمة ضمن جداول تخطيطية دورية، حيث يتم مراجعة نتائج التنفيذ بالمقارنة مع ما هو مخطط لإجراء التصحيح أو التحسين المناسب، ويمكن التعبير عن تخطيط هوشين بأنها توظيف لسياسة الجودة في المنظمة.

إن صعوبة تطبيق هوشين في بعض المنظمات ترجع الى وجوب التطبيق الصارم والالتزام بعيد المدى والدعم المستمر من الإدارة العليا، لأن أهداف الاختراق يجب أن تكون مستقرة لخمس سنوات، ولذلك فإن النجاح باستخدام هوشين يتطلب ضمان تحقيق النتائج المطلوبة من جميع المعنيين بالمنظمة، وتفهمهم للاتجاه البعيد المدى باستخدام معايير قياس تراقب التنفيذ لتضمن استمرارية التحسين المستمر للعمليات الأساسية بالمنظمة.

علماً بأن مفهوم كانري الياباني هو مفهوم إداري يعبر عن تخطيط دوري ويطبق على مستويين[3]:

ما هو رأيكم؟

هذا البند تركته لمناقشاتكم وتعليقاتكم لإغناء هذا المقال…

مع التحية والتقدير لكم جميعاً..

Hoshin Kanri

[2] هوشين كانري في اللغة اليابانية هوشين تعني المعدن اللامع، أو البوصلة، أو تحديد الاتجاه، وكانري تعني الإدارة أو التحكم. وهذا الاسم يوحي كيف يقوم تخطيط هوشين بتوجيه المنظمة باتجاه تحقيق هدف واحد. وهي وسيلة تهدف إلى التعبير وتشكيل الأهداف الاستراتيجية بالإضافة إلى التعبير عن الرؤيا المستقبلية وتطوير وسائل تحولها إلى واقع. ويكيبيديا

[3] للمزيد كتاب: يوجي أكو – هوشين كانري – سياسة انتشار إدارة الجودة الشاملة الناجحة.

[4] حرفيا كايزن تعني كاي “يصبح” وزين “جيد” أي يصبح جيداَ، كايزن هو مفهوم الإدارة الياباني للتحسينات المستمرة بشكل تدريجي، وتعتبر فلسفة كايزن أصل للعديد من المفاهيم الإدارية كدوائر التحكم بالجودة وانشطة مجموعات العلاقات الصغيرة بين العمال، والتحكم بالجودة الشاملة، مع الإشارة الى أن فلسفة كايزن تعتبر أكثر سهولة بالتطبيق من مفهوم الهندرة “إعادة هندسة العمل” كونه يرتكز على مدة زمنية أطول لإحداث التحسين بشكل جذري، للمزيد راجع كتاب: Kaizen – Masaaki Imai

تم بحمد الله اختتام برنامج التعلم التفاعلي الذي قدمه مستشار الإدارة الاستراتيجية المفكر والأكاديمي

زاهر بشير العبدو PTST

بعنوان

إعداد تقارير الموارد البشرية وإجراءات وسياسات شؤون العاملين

Preparing human resources reports and personnel policies and procedures

والذي أقيم في استنبول – فندق #راديسون_بلو_شيشلي بتاريخ 24/05/2021 و إمتد لثلاثة أيام

وقد قام بتنسيق هذا البرنامج السادة

Euro University

من صور هذا البرنامج

حاضر بالبرنامج

مستشار الإدارة الاستراتيجية المفكر والأكاديمي

زاهر بشير العبدو PTST

الرئيس الفخري لـ منظمة الادارة العربية

مبتكر: نظرية MBI©منهجية LeaderShip21© وإستراتيجية ISS©

(مؤلف ، محاضر، مدرب ، استشاري)

*مفكر استراتيجي ممارس معتمد من “Strategic Management Institute”

مؤلف للعديد من الكتب في الإدارة والقيادة الاستراتيجية والتنمية البشرية وبحوث التسويق ودراسات الجدوى الاقتصادية وإدارة المشاريع…

مستشار مساعد لطلبة الدراسات العليا، ومدرب دولي معتمد منذ أكثر من 25 عام.

***

تجدون كتبه على موقع أمازون للقراءة من الرابط التالي: https://amzn.to/3nAlySK

تجدون كتبه المطبوعة على موقع زهرا من الرابط التالي: http://bit.ly/2DxFl08

*

يمكن الانضمام الى مجموعة الادارة والقيادة على الواتس اب من الرابط التالي:

Follow this link to join my WhatsApp group: https://lnkd.in/gpCdaE2

***

للتعرف على أهم روابط نشاطات المحاضر من الرابط التالي:

http://Linktr.ee/ZaherAbdo

الحكومات القادرة

على تحويل أثر عقوبات التقييد و الحظر عليها

-من دول التنمر و الهيمنة العالمية-

إلى حوافز لتَفَوُّق صناعاتها الوطنية البديلة،

هي حكومات ناجحة بامتياز.. زاهر بشير العبدو

Zafer BEŞIROĞLU

#z_b_a #zbesiroglu

www.guidezmart.com

Governments that are able to convert the impact of sanctions and bans, by countries of bullying and global domination, into incentives to boost their alternative national industries are distinguished

successful governments.

Zafer BEŞIROĞLU

#z_b_a #zbesiroglu

www.guidezmart.com

Küresel egemen ve zorba devletlerin yaptırımlarının ve kısıtlama kararlarının devlet üzerindeki etkisini, alternatif ulusal endüstrilerin üstünlüğü için teşviklere dönüştürebilen devletler, mükemmel bir şekilde

başarılı devletlerdir.

Zafer BEŞIROĞLU

z_b_a #zbesiroglu

www.guidezmart.com

التطوير فرصتك الأجدى للتفوق، لكن الصعوبة والكلفة تزداد مع الوقت.

بادر ولا تتردد

Developing is your best chance to Supremacy, But the difficulty and the cost increase within time. Start now and Don›t hesitate

حالة #الابداع النافع هي تلك المتولدة عن #الخبرة الواعية في إستثمار #المعرفة المفيدة والمتجددة.

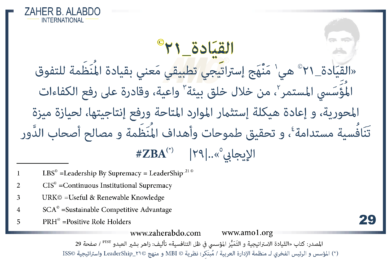

القِيَادة_21© هي مَنّْهَج إستراتيجي تطبيقي مَعني بقيادة المُنَظَمة للتفوق المُؤَسَسي المستمر، من خلال خلق بيئة واعية، وقادرة على رفع الكفاءات المحورية، و إعادة هيكلة إستثمار الموارد المتاحة ورفع إنتاجيتها، لحيازة ميزة تَنَافُسية مستدامة، و تحقيق طموحات وأهداف المُنَظَمة و مصالح أصحاب الدَّور الإيجابي..|29|

(*)ZBA#

—

LBS© =Leadership By Supremacy = LeaderShip_21 ©

CIS© =Continuous Institutional Supremacy

URK© =Useful & Renewable Knowledge

SCA© =Sustainable Competitive Advantage

PRH© =Positive Role Holders

***

المصدر: كتاب «القيادة الاستراتيجية و التَمَيُّز المؤسسي في ظل التنافسية» تأليف: hashtag#زاهر_بشير_العبدوhashtag#PTST / صفحة 29

(*) المؤسس و الرئيس الفخري لـ hashtag#منظمة_الإدارة_العربية / مُبتَكِر: نظرية © hashtag#MBI و منهج © hashtag#21_LeaderShip واستراتيجية ©hashtag#ISShashtag#ZBA